Americans Lose Trillions in Social Security

According to a recent study, retirees will collectively lose $3.4 trillion in potential income that they could spend during their retirement because they claimed Social Security at a sub-optimal time.

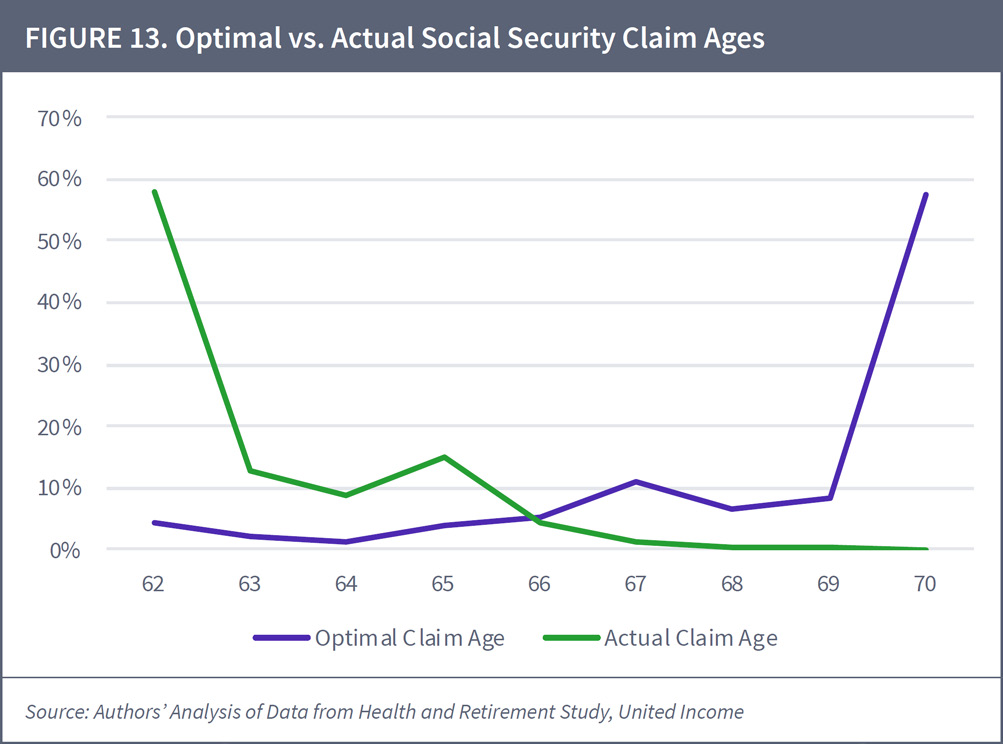

The graph above says it all. The age at which most people claim Social Security (green line) is opposite to the age at which they SHOULD claim Social Security (purple line). In a report from United Income, “The Retirement Solution Hiding in Plain Sight: How Much Retirees Would Gain by Improving Social Security Decisions,” the researchers state, “retirees will collectively lose $3.4 trillion in potential income that they could spend during their retirement because they claimed Social Security at a financially sub-optimal time, or an average of $111,000 per household.”

Nearly all of this income is lost because one or more retirees in a household claim Social Security too early, which means their Social Security benefit is lower than it would be if they had waited. For instance, a person that would receive a $725 monthly benefit if the y claimed Social Security at 62 would see that benefit increase to $1,280 if they had delayed until their 70th birthday, an increase of 77%. Spread out across the population of individuals that are claiming Social Security sub-optimally, those extra dollars add up to a substantial amount of money.

Only 4% of retirees make the optimal claiming decision! The study found that a claiming age of 62-64 is optimal for only about 8% of adults (primarily those with short life expectancies or the spouses of breadwinners)—yet about 79% of eligible adults in the sample claimed at those ages. A claiming age of 70 is optimal for 71% of primary wage earners—yet only 4% of the adults in the sample claimed at that age.

The comprehensive study observed 2,024 households, considering each household’s outside resources, spending, health, and longevity to determine how much income and wealth they would have if they had taken Social Security at the various ages of eligibility.

This appears to be the first study of its kind to consider the impact of claiming age on not just the Social Security income, but other assets and income as well, as optimal Social Security claiming can lead to higher account balances, which in turn generate more income.

Although later claiming typically caused wealth to drop during retirees’ 60s as they drew down their personal retirement accounts, this wealth drop was more than made up for by the late 70s when Social Security income was higher. In order to isolate the effect of claiming age, the study did not consider the effect of working longer, but in real life, a person who decides to maximize benefits by claiming at 70 might choose to work a few years longer, and this would mitigate some or all of the wealth drop in their 60s.

Among those at the highest wealth levels, 99% make suboptimal claiming decisions. Yes, you read that right. 99% of higher-wealth households make suboptimal claiming decisions. While wealthy individuals can perhaps afford to leave Social Security benefits on the table, very few people want to get less than they are entitled to.

Sadly, financially suboptimal decisions add up to a loss of $2.1 trillion in wealth and a loss of $3.4 trillion in income. In its conclusion the report mentions a few ways to deal with this, including:

- Make early claiming an exception, reserved for those who have a demonstrable need to claim benefits before full retirement age.

- Change the way we refer to early or delayed claiming, labeling a claiming age of 62 as the “minimum benefit age” and 70 as the “maximum benefit age.”

- Provide the Social Security Administration with more resources, perhaps in partnership with third-party fiduciaries, to help households determine their optimal claiming age. The authors note, “That limited investment could help recapture some of the $5.5 trillion lost in wealth and income to retirees and the U.S. economy because of the struggles retirees currently face making the right decision.”

We believe that households contemplating Social Security strategies can benefit from a customized analysis that shows the lifetime impact of the various claiming options. With the help and advice of an advisor, you have a shot at being one of the 4% who end up making optimal Social Security claiming decisions. Not only will this increase your Social Security income, it may lead to higher income and wealth from other sources as well.

More nonretired Americans expect comfortable retirement

Meanwhile, a recent Gallup poll found that 57% of nonretired Americans expect they will live comfortably in retirement, a six-point increase in positivity since last year and the highest reading since 2004.

Only 33% of non-retirees see Social Security as a major source of income in retirement (compared to 57% of retirees). Eighteen percent of non-retirees aren’t counting on it at all. Instead, they tend to focus on 401(k)s, IRAs, and other retirement savings accounts as being a major source of income.

While it is likely that Social Security benefits will turn out to be a more important source of income than current non-retirees think, most people will be better off financially in retirement if they work on getting other sources of income together. It is possible some of the 57% of current retirees who see Social Security as a major source of income didn’t feel that way when they were working. But circumstances—the financial crisis of 2008, forced early retirement, lack of savings, disappearing pensions—have turned it into a lifeline.

Elaine Floyd, CFP®, is Director of Retirement and Life Planning for Horsesmouth, LLC, where she focuses on helping people understand the practical and technical aspects of retirement income planning.

Copyright © 2020 by Horsesmouth, LLC. All rights reserved.

License #: 5049052 Reprint Licensee: Rob Williams

IMPORTANT NOTICE This reprint is provided exclusively for use by the licensee, including for client education, and is subject to applicable copyright laws. Unauthorized use, reproduction or distribution of this material is a violation of federal law and punishable by civil and criminal penalty. This material is furnished “as is” without warranty of any kind. Its accuracy and completeness is not guaranteed and all warranties expressed or implied are hereby excluded.